Should I Be Chasing NTFs and DogeCoin?

I am out of breath watching individuals and corporations alike chase the next hot money maker. Car makers are buying bitcoin, friends and family buying Dog coins (Dogecoin) and now we can add digital collectables to the frenzy also known as NFT’s (Non-Fungible Tokens).

If it sounds strange, that’s because it is. People have been paying hundreds of thousands of dollars for NFTs. I read about a Mr. Sheldon Corey from Montreal, Canada, who paid $20,000 for one of these computer-generated art avatars called CryptoPunks. See below:

These babies can be yours for as little $20,000 but if you want the very best pixelated image that money can buy, you can pay up to $2 million for your cryptopunk. Is the image exclusive? Well, no.

Actually, anyone can have an image of the cryptopunk that you might have paid $2 million for. However, you will be the only one that owns the digital rights to it (I don’t get it, either). But I’m feeling the cryptopunk with the hoodie. Which punk has caught your eye?

I bet you’re thinking, “Wow, I’m finally ahead of the game! I know what an NFT is and these digital punks, while insanely priced, are really cool.” I hate to break it to you but you are still late to the party.

CryptoPunks are not new.

They were released by developers Larva Labs in 2017. But the interest in them, that’s very new…so new that in just the last 10 days as I’m writing this blog, crypto art sales have totaled $45.2 million in sales volume. And like every new financial fad, digital art sales seem to have no limit and it doesn’t need to make sense for people to want a piece of it.

The FOMO is Strong in the Universe

How can people actually spend hard-earned money on a digitalpunk or dogecoin? People are not completely crazy. They do it because across the board, early investors make the real money. Whether you’re talking about a pyramid scheme or buying Amazon at $50. If you get to the party early you have a chance to leave with a lot more than you came with.

Gone are the days of contemplation and rational investing. If people catch an inkling of what might be the next hot investment, the masses are jumping in head-first because if it hits, then it was worth the risk. And you have to be in it to win it. Can anyone say “lottery!”

Complacency is No Longer a Bad Word

It was right around the time that Wall Street Bets became a household name that everyone began asking me if I was a part of the Game Stop frenzy or if I purchased any dogecoin? Here is what I think about the digital asset craze: It’s interesting and I love learning about all the potential that these new asset classes have.

However, is crypto a great place to store your wealth? Is it wise to start buying a bunch of digital art and hope that you’re holding the next big thing? For me the answer is a hard no. And that’s because I’m financially complacent right now and I’ve been solidly complacent for the last four years.

What is financial complacency? According to an online dictionary it means showing smug or uncritical satisfaction with oneself or one’s success and achievements.

I’ve had strong and consistent investment growth over the last four years. My investments have held up well against each downturn and my net worth progress proves it. I focus on growing investment income with a portfolio of mutual funds, ETF’s, individual stocks, cash and a base of TIPS (Treasury Inflation Protected Securities). For a little excitement, I invest (almost two years now) a minuscule amount of money into a crypto account.

The money I invest in crypto is divided equally between Bitcoin and Ethereum. I’m not concerned if it goes up or down and the same goes for all of my other investments. I invest automatically and forget about it. I’ve rinsed and repeated this process every month for the last four years and it has worked perfectly, for me.

I can’t imagine disrupting my successful, stress-free path to building wealth, to follow a herd of individuals that invest based on emoji symbols ???????? ????. So, for now I plan to rest in the complacency of my investing success.

Time for the net worth update:

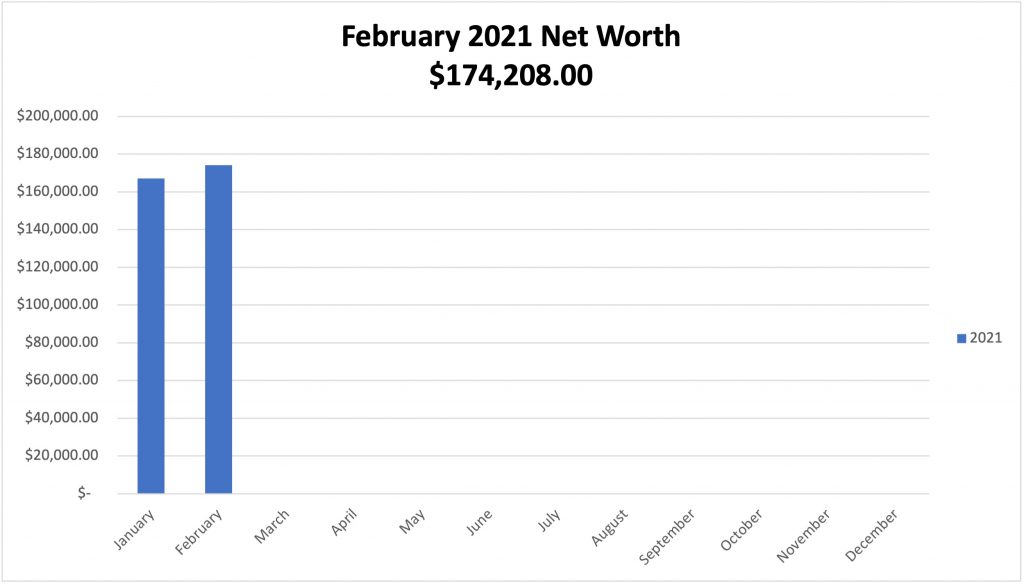

February 2021 Net Worth Update:

The market was off to great start the first two weeks of February, then it was all down hill from there but somehow I managed to improve the old net worth by $7,000 over last month.

| Cash Accounts | |

| Checking | $ 500.00 |

| Savings | $ 5, 625.00 |

| Business | $ 28,752.00 |

| MM/E Fund | $ 28,640.00 |

Taxable Investment Accounts | |

| Ally Brokerage | $28,865.00 |

| Investing MM | $150.00.00 |

| Vanguard | $2,910.00 |

| Acorns | $2,233.00 |

| Tax Advantaged/Retirement | |

| SEP IRA | $12,909.00 |

| Bonds | $20,444.00 |

| Traditional IRA | $43, 180.00 |

| total | $174,208.00 |

- Credit Card: Paid in full every month.

- Checking: Money in and quickly out as usual.

- Savings (P to P): The only money that should go in this account is the $25 that keeps the account free. Unfortunately, the habit of saving is strong and I automatically put a little in when I got paid. If you remember, I was supposed to redirect the $25 I put in this account to my crypto account but when I made the mistake I didn’t bother to correct it.

- Traditional IRA: I’m very happy with this account and will keep doing more of the same, which is buying more shares of solid dividend growth companies.

- Business Account: This account is still a back-up for tax season and remains earmarked for a real estate crash.

- The E/Fund: I still sleep well at night and that means the old emergency fund is doing its job.

- Ally (taxable): CVS and PEG were my February buys. I didn’t add to PEG very much last year, which I regret because they raised the dividend. CVS is new to the portfolio, so I’m working hard to build it up. I’ll continue buying CVS throughout the year

How is your financial year going so far?

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).

I hope all your dreams come true, HAPPY NEW YEAR!