Showing Some Love to the Journey to $200,000

We hear so much about saving our first $100,000. And that’s because it is the most pivotal moment in the life of someone that is ready to seriously build wealth, achieve financial Independence and/or retire (early). It is the mother of all financial steps. It is the hardest step of all the steps. And it takes the longest to do.

Charlie Munger is famous for saying, “The first $100,000 is a bitch, but you gotta do it. I don’t care what you have to do—if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.” But what about the journey towards $200,000? What should one expect at this leg of the journey, how long should it take and what does it represent financially speaking? I couldn’t find anything much written about this part of the journey, so I decided to share my journey and provide a little insight.

In case you’re wondering, the rumors are true. The second $100,000 is definitely easier than the first $100,000. On your way to mile marker No. 2, you will have already done most of the hard work: Getting rid of most, if not all of your debt (except your mortgage), learned to embrace delayed gratification and tweaked your financial strategy to automated perfection. And if that weren’t enough, this is when the power of compounding starts to move the needle for you. Income from my dividends and interest meant that I didn’t have to actually save another $100,000, it was more like $97,000. And in the game of FIRE, every little bit counts.

Newton’s First Law: An object in motion tends to stay in motion…

Not letting up after I reached the first $100,000 was one of the best decisions I’ve ever made. It took a lot of time to create the momentum I have in regards to my income, not to mention the mental and physical energy that it takes to keep all of my projects in the air. I’m almost certain that I wouldn’t have the motivation to pick up where I left off if I stopped or slowed down for any significant amount of time.

It’s Newton’s first law that states, “An object at rest will stay at rest, and an object in motion will stay in motion.” So, I went against the wisdom of Charlie Munger and I continue(d) to put maximum energy towards earning, saving and investing despite already having my first $100.000. More importantly, it is my belief that times have changed and $300,000 is the new $100,000. My advice: Keep your foot on the gas until you have at least $300,000!

The Magic Number?

On my journey to $200,000, I had a strong desire to prove to myself that I could do it again. In the back of my mind, there were doubts. I wondered if it was luck the first time, I wondered worried about job security and I questioned whether I could actually be one of the wealthy FIRE folk that I admire so much? Then one day I hit $175K! Turns out $175,000 was my magic number. That was all the confirmation I needed to prove the first time wasn’t a fluke. Reaching $175K made me confident that I could handle any disruptions to my income and it was proof that I was on track to become one of those “wealthy FIRE folk.” I don’t know if $175,000 will be your magic number, it could be a lot less and it could be a lot more but you’ll definitely know for yourself when you’ve reach that place where you know you can reach your ultimate goal.

Another Day, Another $100,000

On your journey to $200,000, you might notice that your enthusiasm will ebb and flow a lot. I have stretches of not being very enthused with my FIRE journey. I actually went a few days this month without checking my Personal Capital account. For the record, I never missed checking it, multiple times a day, when I was working to reach $100K. Don’t get me wrong, I’m still fired up about FIRE but I don’t have the same level of intensity and excitement that I had the first time around. If I had to assign a number to my FIRE obsession level, I would say I’m at a level 8.

I wonder if the crazed, level 10 person that I was from $0 to $100K will ever come back or if my intensity level will continue to drop as I make progress? With all my debt (except mortgage) gone, all of my investing on automatic and my bills also being paid automatically, the only thing left for me to do is the monthly update of my excel spreadsheet and to enjoy life!

This is probably the leg of the journey where you need to seriously figure out what you’d like to pursue and what you want your days to look like when you reach FIRE.

In the Moment

When I reached $90K on my way to $100K, I was willing to sell clothes, babysit or rent a room out to make sure I not only reached $100,000 but that I did so on or before a pre-determined date. In contrast, when I reached $190,000 I was suddenly exhausted and not willing to do anything extra to reach $200,000 by one of my self-appointed deadlines.

I realized there was no need to work any harder or save anything extra and I’ll still reach $200,000 in two weeks unless the market goes crazy and nose-dives (which is very possible). Assuming I do reach $200,000 in June, it will have taken me a year and six months to go from $100,000 to $200,000 and I don’t want to rush through it. I want to appreciate my effort and reflect on how far I’ve come. I want to live in the moment of this milestone.

Finally, $200,000 may never receive the attention that $100,000 gets. But I think it’s important to realize its significance: $200,000 was my proving ground, where I came to trust my process, I learned that there was a number before reaching $200,000 that allowed me to relax, I learned for myself that $200,000 is lot easier to reach than $100,000 and last but not least, I learned that my greatest level of excitement is probably behind me. That leaves the journey and who I become on this journey the most valuable and most important reason for traveling the road to financial independence.

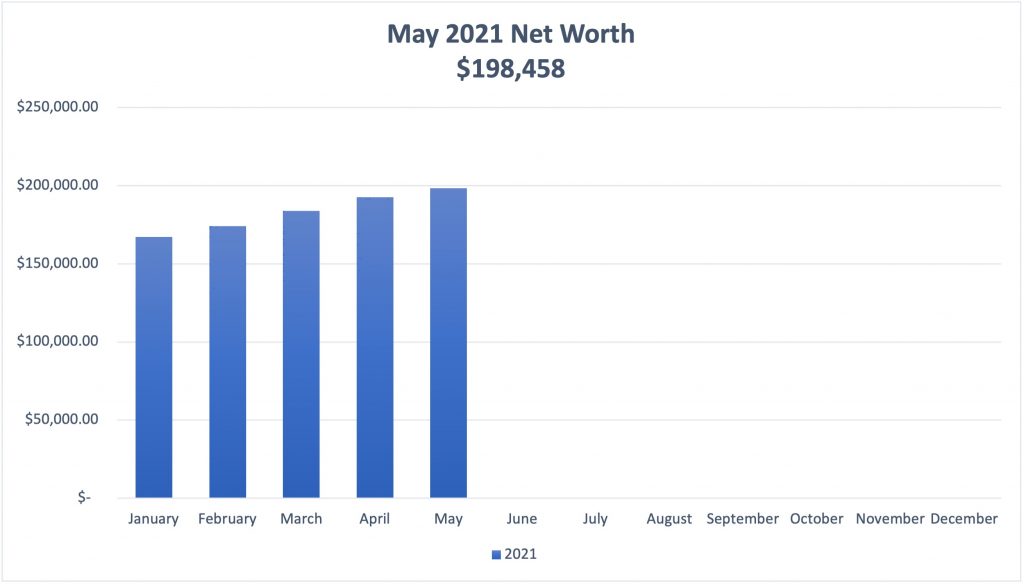

Okay, time for the net worth update:

Cash Accounts

Checking $ 500.00 (no change)

Savings $ 5,900.00 (+$144)

Business $ 32,234.00 (+$1,135)

MM/E Fund $ 30,788.00 (+$760)

Taxable Investment Accounts

Ally Brokerage $ 36,753.00 (+$1,703)

Investing MM $ 100.00 (+$100)

Vanguard $ 3,916.00 (+$376)

Acorns $ 2,550.00 (+$52)

Tax Advantage/Retirement

SEP IRA $15,530.00 (+730)

Bonds $ 21,100.00 (+$200)

Traditional IRA $ 49,087.00 (+$1062)

$198,458.00

Liabilities: Credit Cards: $0.00

- Credit Card: No major expenses this month on the credit card. I was actually below average with my spending.

- Checking: No changes here.

- Savings (P to P): This account continues to be priceless. I used it to pay off that extra-large charge on the credit card last month and paid myself back with interest. It is a pleasure being able to borrow from yourself without penalty or stress of payback. This account is all about having additional options. I sacrificed to create this account when the company I worked for messed up payroll and sent my account into the negative and it took three days to correct the situation. I wanted to defend myself against this and went on a mission to get and keep one month of my salary on hand. It took almost a six months to save a whole paycheck in this account but when the company messed up payroll again (actually three more times) before I left, I was able to just transfer money to cover my expenses. It’s all about creating options for yourself.

- Traditional IRA: Still looking to add an ETF to this account but I haven’t figured out what it’ll be.

- Business Account: This account continues to grow, but I plan to move some of it into Ally next month.

- The E/Fund: Going to throw a portion of this money into a short-term CD with a slightly higher interest rate.

- Ally (taxable): This account exceeded my expectations last month. I didn’t expect to have $35,000 balance until June. Since the bar is raised, I’ll be trying to hit the $40,000 mark by July.

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).