Net Worth Update March 2020

I have to admit it’s not much fun tracking your portfolio when it’s down for the second straight month and the visual that I provided below is stunning. But I’ve managed to stay the course. And while staying the course during this unprecedented moment in history, I’ve learned a few things that I thought I might share.

1. “In bear markets, stocks return to their rightful owners.”~J.P Morgan

This was hard to read especially with so many people that I know personally who having cashed out. There was nothing I could say that would convince them to hold on. Some had to sell at a loss because they didn’t have enough of an emergency fund. Some believed they could time the market and get back in when stocks went even lower. And the rest just wanted out because everyone else was getting out and they believed “this time was different.”

I fell into a couple of those categories back in 2008. However, today I participate in the market as a very informed investor that continues to learn and buy additional shares of stock as prices go up and down. I’m the rightful owner of my stocks and the exponential wealth that goes with being a long-term investor. You are the rightful owner.

2. A six-month emergency fund is no longer enough of a cash cushion.

I’ve watched breadlines form, one third of the country is not be able to pay their rent and mortgage backers tilt toward bankruptcy because like renters, homeowners are no better off and not able to pay their mortgages.

The alarming part is we are only one month into this pandemic. But people are already headed toward financial ruin. This pandemic is going to delay retirement for millions of people and also force millions of people into retirement.

While I’ve been blessed to keep my income (and I certainly have the required six-month emergency fund), I was still left thinking, “what if I were near retirement and/or forced into retirement, would I have enough to last until the economy and stock market recovered?” The answer is no.

I’ve learned that I would probably need two full years of cash to feel comfortable going into retirement and I need to start saving it now.

3. Dividends are more reliable than a job.

I have written several blogs discussing the merits of building and continuing to grow a dividend stock portfolio throughout your working years. I wrote it, so of course I believed what I was saying, but it blows my mind to see just how right was.

As of writing this net worth update, more than 20 million people and counting have lost their jobs. I, on the other hand continue to receive dividends on 20 out of the 21 individual stocks that I own. I’m on track to receive more than a $1,000 in dividends this year.

This is money that, if I needed it, all I would have to do is click a button and those dividends would be deposited into my checking account. Dividend investing is like creating your own stimulus package.

4. Now is the time to build out your side hustle.

If you don’t start building your side hustle during this quarantine, I’m going to go out on a limb and say, you never will. I literally had to write down every detail of what I needed to do to get my side hustle started.

There is still work to do but it has taken four weeks to be able to receive payment (very technical) and I needed outside help. But the worst is over and now I just need a customer. I’m starting this additional hustle while I’m fully employed because I think it’s important to build and get things in place before you actually need the money.

Like an emergency fund, dividend portfolio or your retirement accounts, these are things that need to be worked on immediately because life is, as you already know, very unpredictable.

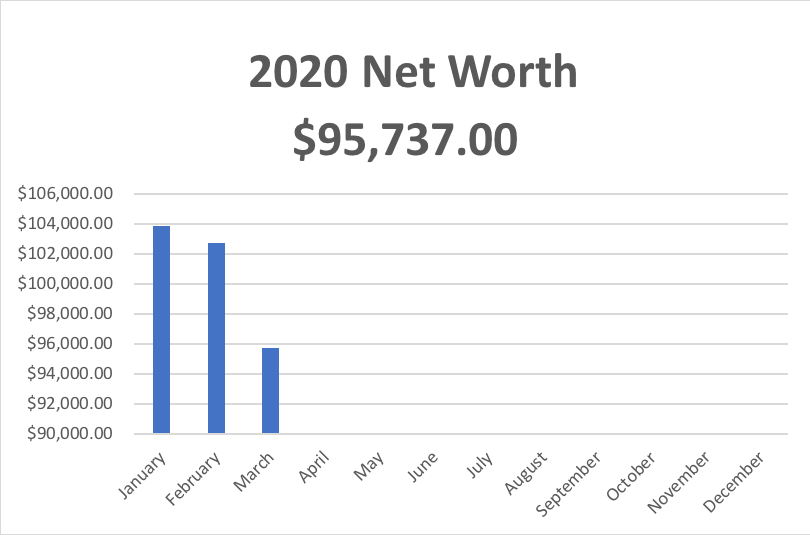

Okay, time for my net worth update.

March 2020 Net Worth Update

Cash Accounts

Checking $ 500.00 (no change)

Savings $ 3,500.00 (- $400)

Business $ 10,641.00 (+$294)

MM/E Fund $ 17,127.00 (+$464)

Taxable Investment Accounts

Ally Brokerage $ 13,004.00 (-$3,007)

Investing MM $ 134.00 (-$25)

Vanguard $ 1,025.00 (-$137)

Acorns $ 844 (-$54)

Tax Advantage/Retirement

Bonds $ 17,707.00 (+$226)

SEP IRA $ 11,446.00 (-$1,875)

Traditional IRA $ 19,809.00 (-$2,511)

$95,737.00

Liabilities: Credit Card: $0.00

- Checking: All savings/bills are automatically deducted from this account. Any money left over after deductions is sent to the emergency fund.

- Savings (P to P): This account is down $400. I had to purchase additional shares of stock. You won’t see buying opportunities like this come around very often.

- SEP IRA: This account took another big hit. My automatic monthly deposit wasn’t enough to keep it even. The bright side is more shares were purchased at a lower price.

- Traditional IRA: This account was also hit hard. It is down more than $2,000 and my automatic deposit was again swallowed up in the downturn. But I managed to make a few buys at basement prices.

- Business Account: This account served its purpose. I had to cover annual business expenses.

- The E/Fund: Haven’t had any reason to hit up the emergency fund. But I may need to keep a lot more than I wanted in this account with all the uncertainty.

- Ally (taxable): Purchased a few shares (UPS, O and NGG) that created $37 in new dividend income.

- Bonds: The current I-bond rate is 2.22% This is still way above what banks are currently offering.

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).