The tax season shook up my personal economy more than the market did this month. Now don’t get me wrong, this has been by far the best tax season that I’ve had in years. In the past, most of my issues came from not being organized with documents on both the business and personal sides. But I worked very hard last year to get really organized and it took most of the stress out of filing my taxes this year.

However, even with all the tweaking I did, two things still managed to slip through the cracks. First, I forgot to pay estimated taxes for the last two quarters of 2017. I’m going to blame it on all the chaos of trying to close on a mortgage. Second, I was scrambling to find $1,568 to put into my personal IRA at the last minute to max the account for 2017.

My goal is for tax season to go by relatively unnoticed. I don’t want to experience any financial turbulence. To remedy any potential turbulence next year. I paid the estimated taxes that I owed for 2017, plus the interest that accrued. I paid my April 2018 estimated taxes early and set up a calendar alert to make sure I pay the next three quarters in advance. I already raised the automatic deposit (late last year) to $455 a month.

Next April will be the first time that I won’t have to add money to max the IRA account for the year. (side note: In 2016 I had to come up with $4,247 to max it out (I did it), 2017 it was $1,568 and unless they raise the limit, in 2018 will be $0.

Okay, time for the net worth and dividend update:

- My net worth took a few steps backwards again because of major dips in the market this month but automatic deposits helped to keep the stock accounts slightly ahead of last month.

- Taxable stocks went up a bit with the purchase of AT&T (T).

- Bonds are doing what they do and will be at the $10,000 mark soon. When the bonds do reach $10,000, I may lower the monthly deposit and redirect it toward debt or the emergency fund.

- The investing fund is running low right now with the purchase of AT&T. I’m currently working out the details on a new side hustle and the income from that should start in May. This means I should be able to buy stock more frequently and still manage to keep the account above $1000 so that I’m always prepared to take advantage of market dips.

March 2018 Net Worth Update

Assets

SEP IRA: $6,795.42

IRA: $8,733.13

CASH: $2,838.46

MM/E Fund: $5,035.25

Stocks (taxable) $4,595.71

I-bonds: $9,054.26

Investing fund: $835.07

Business $3,335.73

Liabilities:

Credit Card: $5,990 @ 0%

Dividend Update:

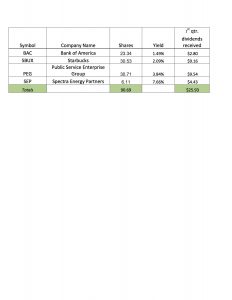

- I added 10 shares of AT&T (T) to the dividend portfolio but the purchase won’t be final until April so, I’ll show it on the April update. If I didn’t mention it before, last year I made $285.52 in passive income (dividends and interest from cash and bonds) but only $43.21 was dividend income.

- Since setting goals promotes better outcomes I decided to set a few modest goals for 2018 dividend portfolio

- Own 7 to 10 different stocks by year end

- Dividends received must be more than all passive income received in 2017 (I’ll need to make at least 253in Dividend income by 12/31/18).