July was a very work-intensive month and I don’t see things slowing down, anytime soon. While I might be burning the candle at both ends, I find myself very motivated. I tell myself that I’m working so that I have a choice as to whether I want to work or not in the near future. I believe things will slow down one day but before that happens I want to be in the best possible position, financially. I believe that we should all strike while the iron is hot.

Seeing Your Hard Work Pay Off

In order for me to know that my hard work is actually worth it, I have to see it. So I quickly decided to increase my savings. It’s my opinion that your money is a physical manifestation of your energy. And because it takes so much energy to bring home a paycheck every two weeks, it makes sense to keep as much of it as possible. My working energy has afforded me the opportunity to have a 65% savings rate.

It seems to me the same discipline that it takes to earn money, is the same discipline that you must tap into to save and invest your money. My plan is to continue my current work schedule and throw as much money as possible into my emergency fund for the next couple of months. Who knows what life will be like after the election?

Lending Money to a Friend Is Dangerous; It Could Damage Their Memory

Update: The friend that I loaned money to remembered to pay me back and is doing extremely well. They were able to pay me back in exactly two months, as promised. I’m very proud of them and proud of myself for pushing through all the noise in my head telling me not to do it.

It wasn’t fun watching my net worth drop but helping someone more than made up for it. That said, loaning money to friends is not something that I would recommend anyone do. This has gone wrong for me more often than it has gone right, which is why I’m so against it. If I think back, this might be the first time that I’ve ever been paid back in full, as promised.

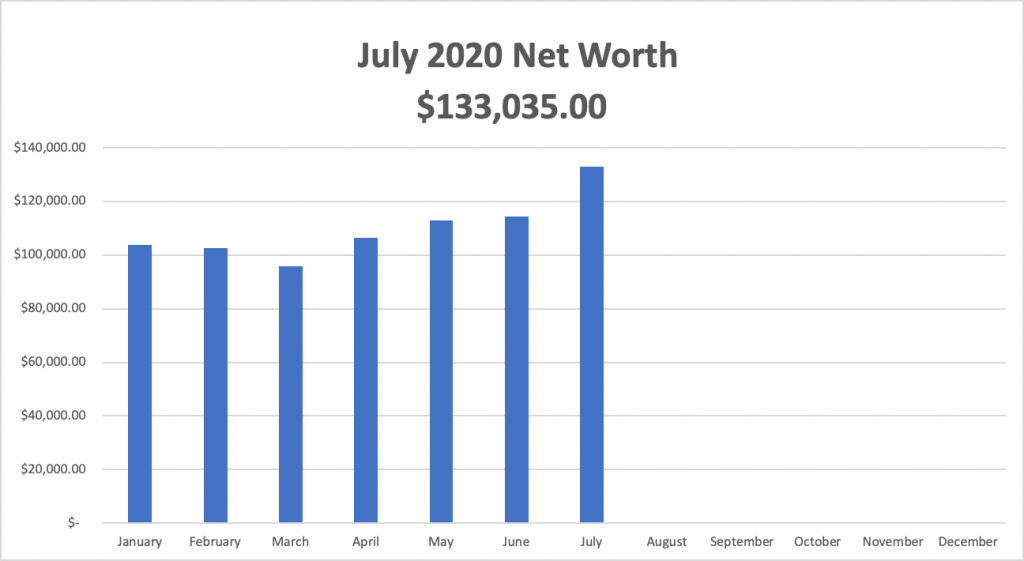

Time for the net worth update:

Cash Accounts

Checking $ 500.00

Savings $ 4,575.00

Business $ 20,290.00

MM/E Fund $ 24,600.00

Taxable Investment Accounts

Ally Brokerage $ 19,096.00

Investing MM $ 243.00

Vanguard $ 1,711.00

Acorns $ 1,246

Tax Advantage/Retirement

Bonds $ 18,728.00

SEP IRA $ 15,753.00

Traditional IRA $ 26,293.00

$133,035.00

Liabilities: Credit Cards: $0.00

- Credit Card: Balance is always paid in full at the end of the billing cycle

- Checking: Bills remain low, not eating out and no gym membership.

- Savings (P to P): This account will soon hit $4,700. I plan to take the $200 and buy stocks. I want this account to stay around $4,500.

- SEP IRA: Caught a nice bump from the stock market this month and I hope it continues.

- Traditional IRA: July is the month that this account finally stopped moving sideways and down.

- Business Account: This account is back to where it should be at this point since receiving the money I loaned.

- The E/Fund: To my surprise, the interest rate remains at 1% and I will continue to plow money into this account for the next few months.

- Ally (taxable): Purchased a few shares of SPG, O, MAIN and MDT.

- Bonds: The current I-bond rate is 1.06%. This is now higher than most online HYSA’s

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).

(None of this information is intended to be investment advice and is for entertainment purposes only).