What’s Your Financial Tipping Points?

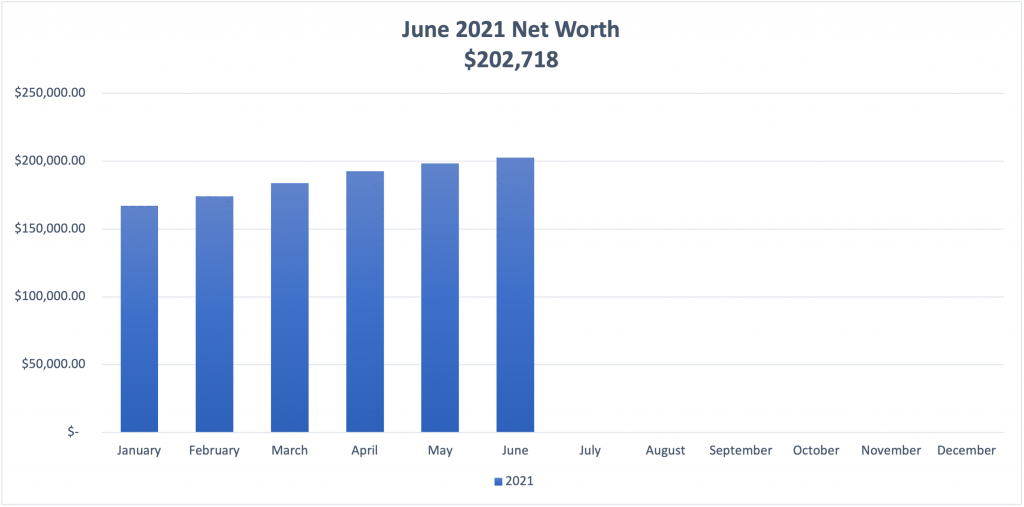

Spoiler alert! I crossed the $200,000 milestone and my journey to $300,000 has officially begun. Unfortunately, my milestone celebration didn’t last long. Two weeks after reaching $200K, the market began to drop slowly for an entire week. I wondered if this was the big crash that all the “experts” said was looming?

Turns out it wasn’t “the big crash,” but my portfolio had still taken a hit. Not confident that my portfolio would climb back to $200,000 by the end of the month, I couldn’t bear to look at it anymore. I needed a distraction from all the financial news and market predictions. Also, I needed to figure out the source of my new-found anxiety. So, I did a deep dive into my thoughts around this $200K milestone and why going below it seemed to bother me more than I realized.

A Moment

The market started dropping on Monday, June 14 and by Wednesday, I was down a little more than $5,000. It was obvious that I was more emotional about reaching and staying above $200,000 than I ever was about reaching and staying above $100,000.

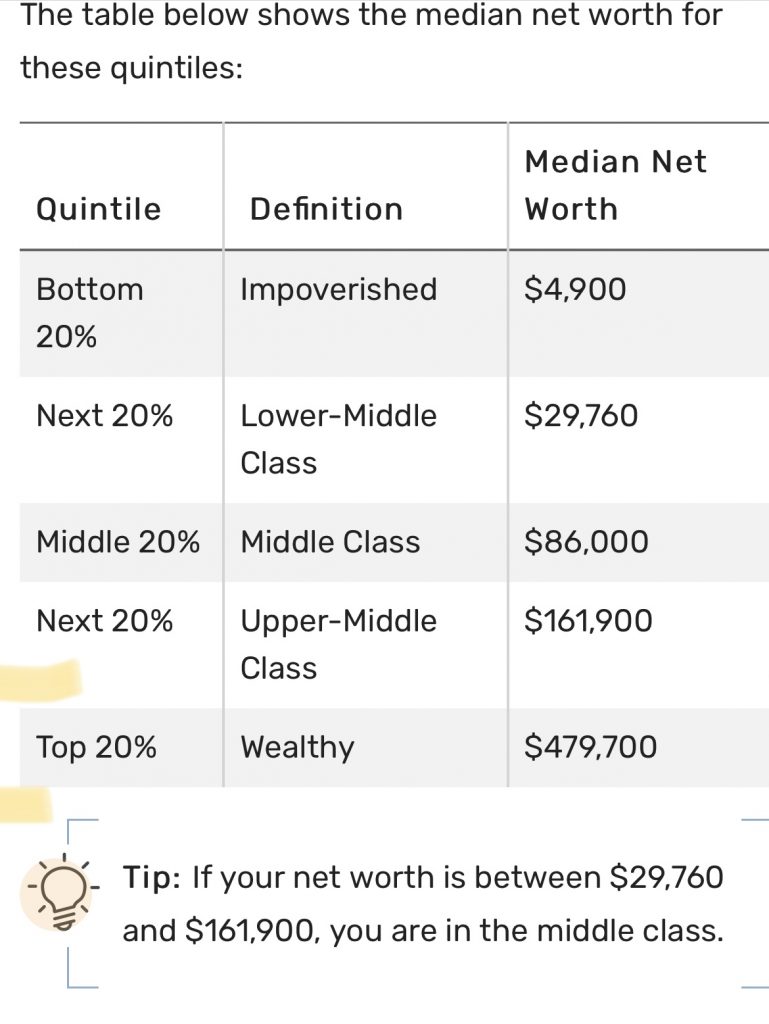

Turns out, $200K represents a strong line of demarcation between poverty and being firmly upper-middle class to me. It takes a lot of hard work to build a significant net worth: Educate yourself on all things financial (and never stop), change your mindset from consumer to investor, discipline yourself (in every area), which leads to consistency and great results.

However, if you come from poverty or you’ve witnessed it up close, then you know that even if you put in the work, the reward isn’t always an elevator ride to the top. In fact, it’s just the opposite.

When you’re poor, you tend to stay poor. As for the middle class, it’s shrinking, which means they’re slowly growing poor. The only class of people that are growing and building on their net worth are the upper-middle class and the wealthy. And that’s why I had so much anxiety about staying above $200,000.

Movement Between the Classes

A lot of pride and identity rides on the label “middle class” but the truth is middle class looks a lot like poor in real life. So, the government has assigned labels that make people with a “net worth” of $29,000 feel superior to the people with the $5,000 net worth. But both are barely surviving and will have even more in common over the next 10 years.

I have friends at both ends of the income spectrum. And I’ve watched a few of them make it from poverty to middle class and watched others in the middle class slip into poverty. On the other hand, I’ve never witnessed the upper-middle class and wealthy slip all the way to poverty. Not once. Of course, there are anomalies. But I’ve only read about them. For the most part, the wealthy stay wealthy and the poor stay poor…whether we like it or not.

Tipping Point

I believe there are personal finance tipping points. You probably haven’t told anyone or spoken them out loud, but you have them in the back of your mind.

What are financial tipping points? They are the points of no return. The balance on your credit cards that you know you can’t go over or else your finances will flat line. That’s a tipping point. Emergency savings represents a tipping point. You have X amount of months before your emergency fund runs out and if it does, you know your financial ship is taking on water and you’re going down fast.

On other side, wealth accumulation also has a tipping point. Once you have collected enough assets that pay you, you don’t really have to worry about going to the poor house if you lose your job. An upper-middle class or wealthy person can survive life’s storms without decimating their net worth and slipping into poverty. And if life goes as planned for the upper-middle class, they simply continue to grow wealthier and wealthier until they’re officially rich.

According to the chart above, I’m upper-middle class and that number is supposed to represent financial security. It doesn’t for me. I still feel financially vulnerable. If I could slip down to $195,000, how easy would it be to slip below $167,000 and $86,000? You get where I’m going. So my question is does that feeling of financial slippage and vulnerability ever go away? Is $479,900 the magic tipping point number where you never have to worry about sleeping in a tent?

Perhaps sleeping in a tent is a bit much. But here’s what I think, the tipping point happens when you start passively making at least half of what you need to survive each month. So while I’ve come a long ways, I still have a lot of work to do. Are you near a tipping pointing negatively or positively?

The Goal

I don’t need to tell you that poverty (lower middle-class) is painful. Therefore, my goal (and hopefully your goal as well), is to create a chasm between me and poverty. You do this by keeping your expenses as low as possible, saving more than you spend, investing the difference and finally, making it a rule that when you buy something it’s either going to be paying you or appreciating.

Okay, time to see how close I am to the $300,000 milestone.

$97,218.00 to reach $300K

Cash Accounts

Checking $ 500.00 (no change)

Savings $ 6, 000.00 (+$100)

Business $ 33,004.00 (+$770)

MM/E Fund $ 31,423.00 (+$635)

Taxable Investment Accounts

Ally Brokerage $ 37,400.00 (+$647)

Investing MM $ 100.00 (+$100)

Vanguard $ 4,500.00 (+$584)

Acorns $ 2,600.00 (+$50)

Tax Advantage/Retirement

SEP IRA $16,090.00 (+560)

Bonds $ 21,381.00 (+$281)

Traditional IRA $ 49,720.00 (+$633)

$202,718.00

Liabilities: Credit Cards: $512.00

- Credit Card: I did a lot of food shopping this month. Perhaps I was bored, but I definitely plan to cut back next month (paid in full).

- Checking: No changes here; just money for bills going in and out.

- Savings (P to P): This account has turned into a paranoid cash hoard and I’m not ready to part with it.

- Traditional IRA: Still haven’t decided what ETF to add here. For now, I’ll just keep adding to my current holdings.

- Business Account: This account is turning into another cash hoard. I’ll be transferring a bit to my brokerage throughout July.

- The E/Fund: I got busy and didn’t take advantage of a 0.70% CD offering.

- Ally (taxable): If I’m able to stop my cash hoarding ways, this account should be at $40K by September

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).