There is Hard Work Ahead For Us All!

Welcome to the first net worth update of the new year. And if January is any indication, we should all fasten our seatbelts because it’s going to be a bumpy ride year.

Nothing seems smooth politically, pandemically, racially or economically. However, I often hear people say that Pres. Joe Biden and Vice President Kamala Harris (yes, I enjoyed typing her name and title) have their work cut out. But don’t we all have our work cut out for us? Unless, the plan is to sit back and wait for stimulus checks and unemployment extensions.

Unfortunately, that seems to be the plan for many. Going back to school or picking up new skills to avoid being subject to dying industries and low-wage jobs is not something that seems to interest most people. Enrollment in four-year colleges and universities, two-year community colleges and trade schools have continued to decline. Where do we go from here if “we the people” don’t want to put in the work?

The purpose of this blog

I don’t think I need to say it, but I will. I post my net worth for two reasons: Motivation and accountability. It is my hope that by watching the slow and steady progression of wealth building in real time will be motivating enough to take you on a path that leads to your own financial progress and freedom. And in return, I’m held accountable by having to report my successes and when I miss the mark. When sharing my personal finances doesn’t fall into those two categories it’s a problem and I will probably no longer do it.

“Comparison is an act of violence against the self.” -Iyanla Vanzant

Recently, I had an old, in-and-out-of-my-life kind of friend (for privacy let’s call them Isabelle) come to me with their financial issues. It is not the first time Isabelle has come to me for advice. But she is the kind of person who literally walks away from the mirror and forgets what she looks like.

I’ve spent hours in the past going over what she needs to do, but either she never does it consistently or she never implements the advice given to her. It also seems to me that she was comfortable hoarding money in a savings account for the last 15 years and not investing a single dime of it as long as she believed herself doing better than everyone around her (but time does fly).

It’s Not Where You Start, It’s Where You Finish

I used to be the kind of person that would never stay at a job very long and seemed to always be drifting and trying to find my way. For a better picture, Isabelle stayed at the same job for more than 15 years and lived in the first home she bought for just as long.

The truth is, I was never the kind of person that could stay at one job. Doing the same thing for decades at a time seemed like a self-imposed purgatory. I’m a free spirit who wants to live and experience life every single day, not just twice a year on some rote vacation.

Also, I quietly want the finer things in life. That means, I must have a nice car and I must have an above-average place to call home, which can be very expensive and create regrets if you don’t learn to get your financial ducks in a row.That desire set me on a mission to get my financial ducks in a row.

I got smart, very smart, financially. Then I started putting my knowledge into action. When my financial smarts started compounding, I realized that I had accomplished in four, focused years what Isabelle hadn’t accomplished in 15 years. I focused on self-mastery, which means I focused on doing all the things that unsuccessful people “don’t feel like doing.” (Note: Most successful people don’t like doing them, either. They are successful because they do it anyway).

Once I mastered myself, I turned my attention and discipline to wealth building.

As a result, I have passed Isabelle financially. And I did it my way, not following societal norms or waking up to find I played the lead role in a Stepford nightmare of a life of my own doing.

As I was talking to Isabelle about the things I had learned, she asked me, politely, what was my net worth. What?! I threw out a number and I could hear Isabelle dragging out her long, wooden, mental, measuring stick and comparing herself to me.

Big mistake! Comparing yourself, in any capacity, only serves to make you perhaps feel better if you have more than someone or feel worse because you have less. But it still doesn’t answer whether you are living up to your full personal potential. There will always be millions of people that have more than you that are sad and there will always be millions of people that have less than you that are happy.

What You Focus on Expands

My hope is that Isabelle will focus on herself in this old-new desire to get her financial life in order. What someone else has should not be your measuring stick of financial or life success. Whether someone else has reached their goal or not, won’t bring you any closer to reaching yours.

Know exactly what you need and want to make you happy and let that be your measuring stick and guide.

Okay enough of that, time for the net worth update:

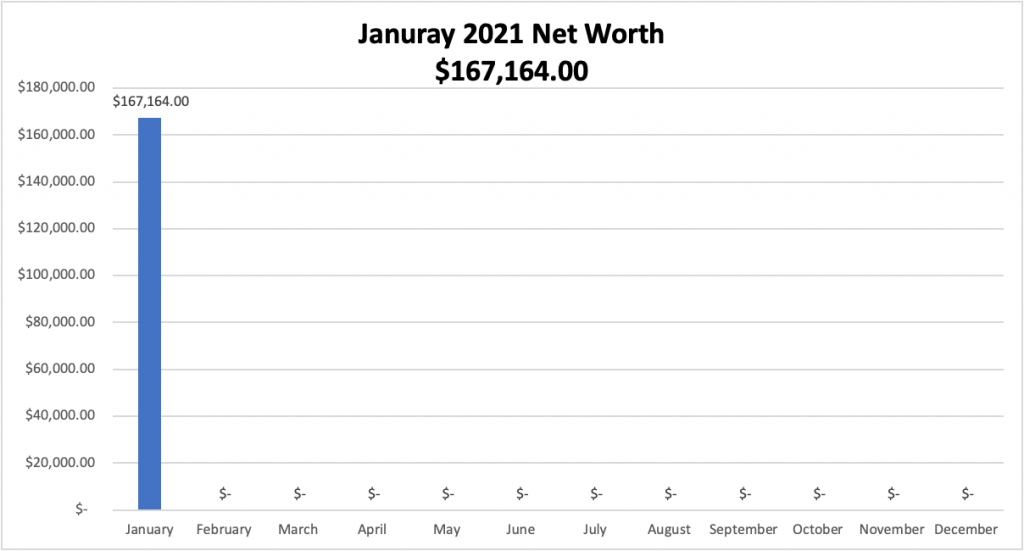

January 2021 Net Worth Update

Cash Accounts

Checking $ 500.00 (no change)

Savings $ 5, 550.00 (+$300)

Business $ 27,005.00 (+$250)

MM/E Fund $ 28,013.00 (+$513)

Taxable Investment Accounts

Ally Brokerage $ 27,123.00 (+$625)

Investing MM $ 200.00 (+$100)

Vanguard $ 2,581.00 (+$19)

Investing App $ 2,130.00 ($157)

Tax Advantage/Retirement

Bonds $20,223.00 (+$200)

SEP IRA $12,046.00 (+$448)

Traditional IRA $41,793.00 (+$212)

$167,164.00

Liabilities: Credit Cards: $0.00

- Credit Card: Paid in full every month!

- Checking: No changes

- Savings (P to P): ($5500 was the goal) I reached my goal for this account and so moving forward any money that I would have put in this account will now go towards buying crypto. I’ll divide the amount (it varies) evenly between bitcoin and Ethereum. This is another example of the blog holding me accountable, I had forgotten this was my plan. I won’t be tracking my crypto on this blog. All the tracking I currently do is enough work and I don’t want to add to it.

- Traditional IRA: This account dropped by more than a $1,000 the first week of the month. I’m actually surprised that it wasn’t worse.

- Business Account: This account is now serving as a back-up for tax season and will be used to purchase an asset sometime in the future.

- The E/Fund: On schedule to reach a new milestone over the next few months. Some might say I have too much sitting in cash. But it helps me sleep better at night, so I’ll continue to fund the account until I feel that it’s time to stop.

- Ally (taxable): The market is creating wonderful buying opportunities of which I will continue to take advantage.

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).

Start building the future you want today!