I’ve been thinking about money and wondering if enough will ever be enough, for the middle class, millionaires and billionaires. If you’re a longtime reader, you’ll notice that I haven’t created a financial destination number. I’ve toyed with saving the $1.3 million experts say is needed to be financially secure. But I don’t believe I need that much.

They say, you never can have too much money. I once believed that, too. Not any more.

Have you taken a look at the state of the world lately? I believe the world is where it is and has reached a tipping point economically, politically, racially and environmentally because enough of anything is never enough. (This brings to mind Mary Trump’s book, Too Much and Never Enough).

Over the weekend I binge-watched this season of Bravo’s, Million Dollar Listing Los Angeles. I watched the real estate agents work hard to sell $25 million homes that were never lived in because the owners didn’t like the view. I watched clients turn down a $15 million homes because it only had a 10-car garage and he needed more parking. The majority of the agents on the show live in $10 and $20 million homes and their assistants are striving for the same level of excess. My question: When will the insatiable desire for more and more and more end?

A study was done on a group of people who all inherited $1 million or more. Members of the group were asked, how much money they would need to feel as if they had enough. Every last person in the group said they would need double the amount they received to feel secure.

That group included people who had received over $50 million. Even they said they needed twice as much. It didn’t matter if they inherited $1 million, $12 million or $50 million, everyone in the group needed double what thy received to live “comfortably.” It is not lost on me that wealth is all relative. But again, will we ever admit that enough is enough?

One of my favorite blogs, A Purple Life, recently retired. She took readers on her journey from start to finish. She worked hard and saved harder for nine years. Along the way, she figured out exactly how much she needed to cover her living expenses. On October 1, 2020 at the age of 30, she will retire on approximately $550,000.

She is going to travel and live in work-free bliss, essentially forever. A Purple Life also made the decision to leave on that date even if she fell short of her half-a-million-dollar goal.

I’m not saying her journey would work for everyone, but she figured out that she didn’t need a million-plus dollars to enjoy and live life on her terms.

If you want to live life on your own terms, the next time you sit down to figure out how much you need try trimming the fat. Do you need the $10,000 vacation every year, the luxury car and all 200 cable channels? Perhaps before you figure out your retirement number or how much money you need to feel secure, you should spend spend some time getting to know who you are, what you really want and what brings you the most joy. You’ll find that those things probably don’t require an installment plan.

I don’t want to be responsible for more than what my passive income can cover. So, I’ll also be doing a bit of soul searching and figuring out what I need to walk away from all of my work obligations. I’ll be sharing that number in a future blog.

I have decided I’m not willing to work five extra years to reach a bigger number. Enough will be enough.

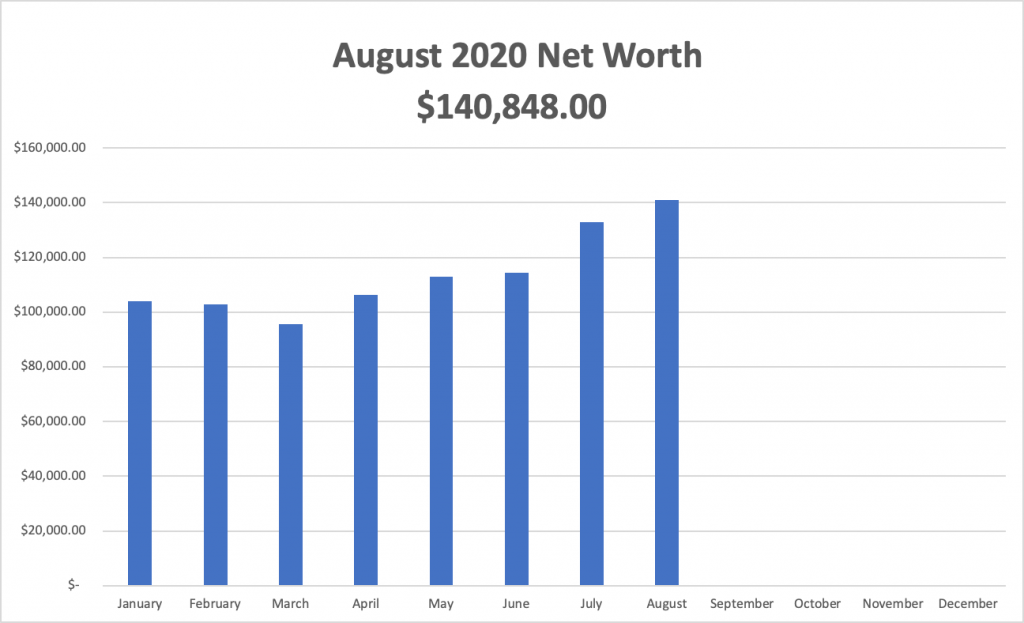

Okay, time for my August net worth update:

August 2020 Net Worth Update

Cash Accounts

Checking $ 500 (no change)

Savings $ 4,650.00 (+$75)

Business $ 23,000.00 (+$2,702)

MM/E Fund $ 25,100.00 (+$528)

Taxable Investment Accounts

Ally Brokerage $ 20,300.00 (+$1,204)

Investing MM $ 443.00 (+$200)

Vanguard $ 1,857.00 (+$146)

Acorns $ 1,370 (+$124)

Tax Advantage/Retirement

Bonds $ 18,928.00 (+$200)

SEP IRA $ 16,900.00 (+$1,147)

Traditional IRA $ 27,800.00 (+$1,507)

$140,848.00

Liabilities: Credit Cards: $0.00

- Credit Card: Paid in full at this point

- Checking: The old gym membership is back. I’m not sure if I’m taking it into next year.

- Savings (P to P): This account is capped at $4,500 but when it hits $4,700 I’ll take the $200 and buy stocks

- SEP IRA: Not a great month for the old IRA, but my automatic deposit held it up

- Traditional IRA: This account has been moving sideways for the past month

- Business Account: No big expenses this month. I will probably go stock shopping next month

- The E/Fund: Interest rates have dropped again, down to 0.80%

- Ally (taxable): Added a new ETF that pays monthly: SPHD

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).

(None of this information is intended to be investment advice and is for entertainment purposes only).