I’m always so optimistic about the first quarter and all the progress I plan to make. One would think that I’d have learned by now that the first quarter is usually the most busy and expensive time of the year for me. With taxes to file, accountants to pay and quarterly taxes due, I’m usually too distracted to execute all the things I planned to do in my portfolio.

While my savings are on target, as it should be because it’s on automatic, the passive income is lagging. My goal is to double the amount received last year ($234.47) in dividends and right now it’s not looking good.

I’m not entirely to blame. The stock market has been raging and all the stocks that I wanted to buy in the first quarter (PG, O, PEP, DAL and IBM) just keep going up. The upside to all this is that it has forced me to research new buying opportunities.

I came across (IRM) REIT and will be adding it to the to the C to C portfolio soon. Also, I plan to bite the bullet on the others and start averaging in on small market dips.

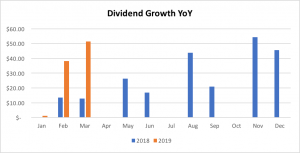

The chart below shows my dividend progress year over year:

This is the year of filling in the off months (Jan, Apr, July, and Oct) of the dividend portfolio. (so I can receive dividend monies every single month).

I hope to make real progress in July and October with the purchase of LTC, PEP and O. But the other side of the equation is coming up with enough cash to make the progress I want without impeding the progress I’m making in other areas.

I’m often tempted take from other areas. I automatically deposit $50 a week to purchase stock. And if I have any unexpected income or I’m able to save money not buying lunch or by lowering bills in other areas, I put that into the pot, too.

Having made the decision to pay down and payoff the mortgage has made resources available for stock purchases very limited. But I’m still optimistic and excited to see what kind of progress I’ll be able to make by year end.

Okay, time for the net worth update.

April 2019 Net Worth Update

Assets

Cash Accounts

Checking $500.00

Savings $4,001.00

Business $3,070.00

MM/E Fund $11,400.00

Taxable Investment Accounts

Ally Brokerage $9,705.00

Investing MM $692.00

Vanguard $415.00

Tax Advantage/Retirement

Bonds $15,011.00

SEP IRA $10,163.00

Traditional IRA $17,238.00

Total $72, 198.00

Liabilities:

Credit Card: $1,072.00

- Checking: Nothing new happening here. Just money going in and coming out like clock- work.

- Savings (P to P): This account is at a comfortable level. I topped it off with my tax return. I won’t be adding anything to it other than the $25 automatic deposit that keeps my account free of charges. This account has no interest at 0.04%. I keep this money here to avoid having to touch my emergency fund.

- SEP IRA: The market did well in March and this account reaped the benefits.

- Traditional IRA: The market gave this account a boost. Also, I now deposit $500 a month to meet the new $6,000/yr. maximum.

- Business Account: I had to pay the accountant and 2019 quarterly taxes so this account has reached a new low.

- The E/Fund: I haven’t had any reason to hit up the emergency fund. As a matter a fact, I added a few bucks to this account with the tax return I received.

- Stocks (taxable): With stock prices rising, it has taken longer for me to make purchases. But when my raise kicks in next month, dividend growth will pick up in the second half of the year.

- Bonds: This account is at a new high and bringing in close to $30 a month in passive income.

- Ally Investment: With stocks being so high, I’ve been sitting on the sidelines and this had allowed the account stack up a little. I also dropped a few extra bucks in this account thanks to my tax return.

- Credit Card debt: Currently stands at $1,072, which I’m not okay with. A recent and unexpected drop in business income will leave me paying this off in multiple payments instead of the one lump sum I expected. You know what they say, don’t count your chickens before they hatch. I should be able to pay it off before any interest is accrued, but not comfortably.

I hope that you will use this new month to jump on this wealth-building ride. There is no better time to start than now. And if you are already on your wealth-building journey remember:

“It is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).”