New Investors: Focus on Earning and Saving, Not the Crazy Market!

Economically, the ???? has hit the fan. I thought January was a rough month. But February was downright nasty. I’m currently on a 22-month net worth increase streak that I thought would end in January and knew for certain would end in February. But somehow, albeit a very small increase, my net worth has now gone up for 23 months straight!

I’m creeping up on my previous streak of 26 months, which came to an abrupt end March 2020. Like the first streak, I also attribute this one to a high savings rate. How much I save is still something that I focus on because I’m still very early (five years) into my FIRE journey.

Saving My Way to a Zero Net Worth

Depending on the level of financial independence that you’re striving for, the journey can take anywhere from 10 to 15 years. However, it doesn’t take that long for you to start reaping the benefits of your wealth. I felt powerful when my net worth hit zero. Yes. $0. It was the first time that I didn’t owe anyone a portion of my paycheck, my revolving debt was finally gone. My money would only go toward building my future, which at the time meant a six-month emergency fund and buying a home. I saved and saved and saved. I saved. And I exceeded my own expectations.

For the first time (in 2017), I had maxed out my IRA and I had a few individual stocks and ETF’s that I infrequently purchased. (I hadn’t fully bought into dividend growth investing yet). But my net worth quickly hit $40K and I knew that I was on to something. In a year, I had enough for a down payment on a home and I had a two-month (and growing) emergency fund. I was confident that I was doing something right and my plan was to rinse-and-repeat my way to $100K.

Saving Is the Engine Behind a Budding Net Worth

Between $50K and $75K, I stepped up my investing. I had been doing a lot of reading and it clicked that I needed to get compounding on my side as quickly as possible. (FYI…It is impossible to save your way to financial independence).

I officially understood the power of creating a compounding stream of dividend income for my future self. By the end of my first year of consistently buying dividend-paying stocks and ETFs, I had made a whopping $234.42 in dividends and approximately $1,100 in stock appreciation. I was speeding toward the sacred $100K net worth but it certainly had nothing to do with my investment returns.

My savings rate was around 35% and I was working hard to hit 50%. In the third year of my FIRE journey (2019), three amazing things happened. In December of 2019, my net worth finally hit $100K (exactly $101,367. 00), I had nearly doubled my dividend income over the previous year receiving $447.76 in dividends, and I was finally saving around 50% of my income. My equities had appreciated and, combined with dividend income, was perhaps responsible for 5%-10% of my newly minted $100K net worth.

Approximately 90% of all the wealth I had accumulated across my portfolio (savings, retirement, brokerage and bonds) was money that I worked for, saved and invested. Compounding was working but not nearly as hard as I was. Fast forward to 2021 and I made nearly $2,000 in dividends last year. I have thousands of dollars in appreciation but the amount I save still has more of an impact on my net worth than market returns.

Last year, I did have a couple of months where the market came close to matching what I put in but until it happens consistently, I’ll continue to work hard on the earning and saving side of things and wait for compounding to relieve me of my duties in the next three to four years.

The moral of the story, you and your hard work will be responsible for the majority of your net worth growth at the start of your financial independence journey. Don’t waste any time worrying about the returns you get from the market, especially when you have less than $100K (and perhaps even when you have $300K-$400K). Just keep your head down and focus on your earnings and your savings rate and remember a 50% savings rate is the sweet spot.

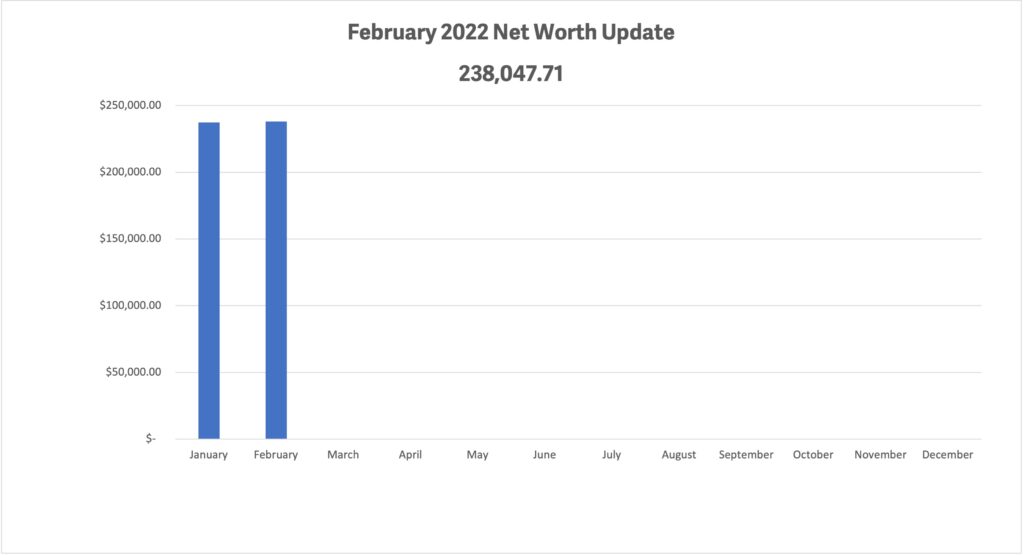

Okay, time for the February net worth update:

Financial independence has proven to be a game of inches lately. But if you’re on this journey with me, you appreciate all your gains. My net worth increased by $582 over last month. Not the big increases that I’d gotten used to but certainly something to be happy about as the streak lives on. Again, the market was ridiculous this month and that gain is just me constantly dumping cash into my brokerage account throughout the month and buying whatever went on sale in my portfolio.

As you can see, I’m seriously behind my goal of $250K by the end of the first quarter. Hopefully, things will start to improve as the year goes on. Perhaps I’ll reach my goal in the second quarter. In the meantime, I’ll continue to focus on saving and investing and with my next goal.

Now onto the passive income that I’ve dedicated to my future self:

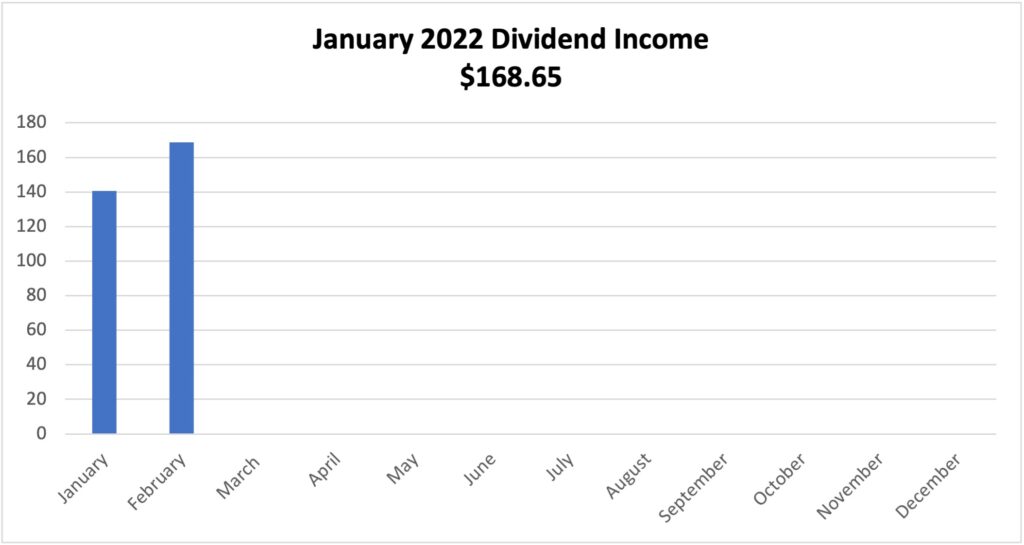

February has slowly turned into a strong dividend-paying month for me. Seeing it on the chart below allows me a visual of just how far I’ve come (and I love charts and graphs). To add some perspective, last February I didn’t even cross $80 in dividends. It took most of last year to build up to this point.

This year, I’m working on the first month of each quarter (Jan., April, July, Oct.) because companies don’t usually pay during those months. My plan is to continue looking for strong companies that I can add to those months. But for now, I will just add to the positions that I currently own to bring them up.

My goal is to eliminate significant drops in my dividend income from month to month when I’m living on this stream of income. I’ve seen dividend portfolios with a $1,200 payout one month and $198 the next. I would like to be a little kinder to my future self than that. Here are all the individual stocks and ETFs from my taxable brokerage account that paid me in February (Retirement accounts are not included):

| February Dividend Payout: | |

| SBUX | $18.99 |

| T | $56.31 |

| PG | $11.6 |

| JEPI | $14.47 |

| O | $12.33 |

| MAIN | $8.8 |

| APPL | $1.11 |

| OHI | $30.85 |

| CLX | $5.8 |

| CVS | $8.39 |

| $168.65 |

Remember, it is a fight to build wealth no matter where you are in the process. Everything around us conspires to take money out of our hands. But you must fight the good fight. Continue to save, invest, and grow your net worth even when it seems impossible. Save your pennies (copper) until they become dollars (cotton).